The upcoming OPEC+ meeting on June 1 is unlikely to bring major surprises, as Allianz Trade expects the current supply restrictions to be maintained. Recently, oil prices have been on a rollercoaster, surpassing $90 per barrel in early April due to rising geopolitical tensions in the Middle East, before dropping to around $82 per barrel amid concerns about demand and Fed interest rates.

Looking ahead, Allianz Trade forecasts that oil prices will average $84 per barrel in 2024, before slightly declining to an average of $81 per barrel in 2025.

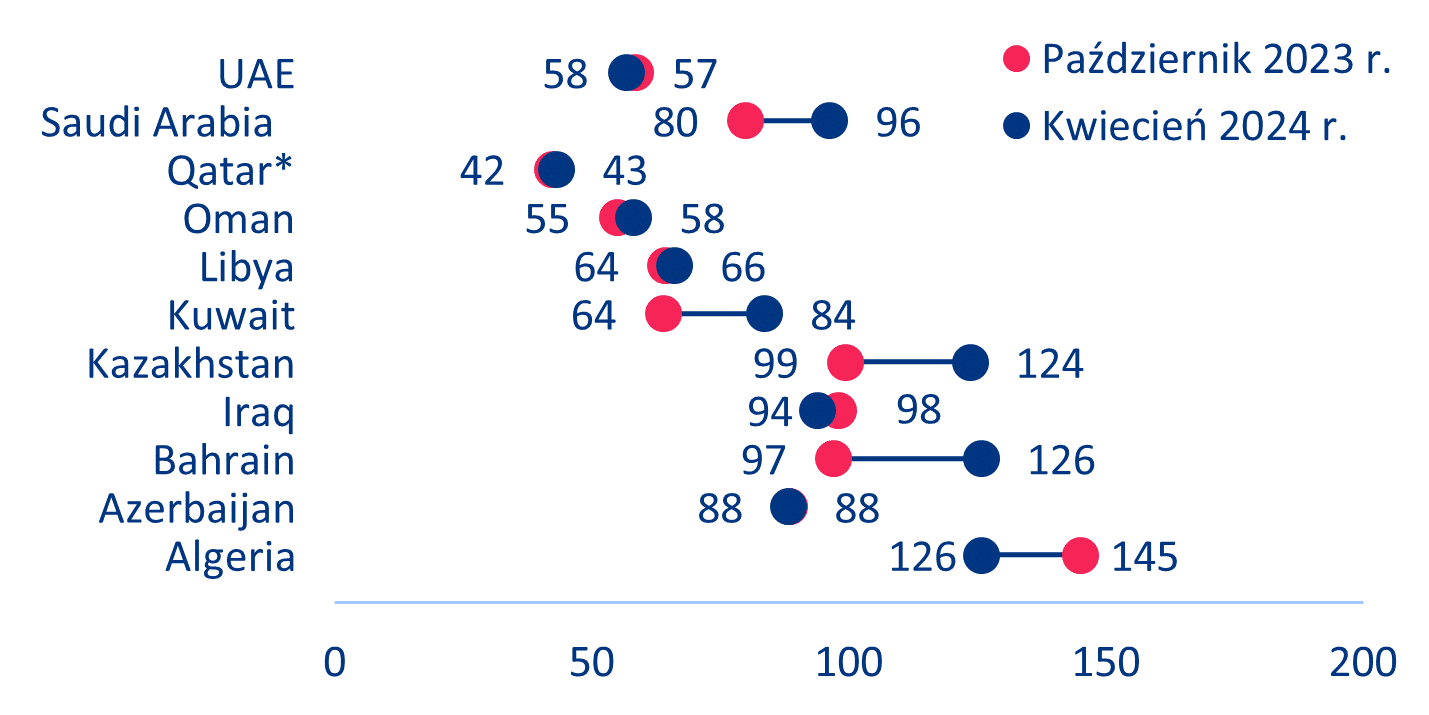

The upcoming OPEC+ meeting on June 1 is expected to be uneventful… Markets will be closely watching the outcomes of this week’s meeting of the Organization of the Petroleum Exporting Countries (OPEC) and its partners, known as OPEC+. The group is likely to extend its production cuts by 2.2 million barrels per day (bpd) to keep prices above $80 per barrel. However, non-OPEC production is offsetting OPEC+ cuts, and US production remains at record highs, despite some weather-related downtime, keeping price increases in check. Saudi Arabia, which has made the largest cuts, needs oil prices close to $96 per barrel (up from a previous estimate of $80 per barrel) to finance its ambitious transformation plans (see Chart 1). However, if the country returns to its previous production level (close to 10 million bpd) by next year, its breakeven price could drop to around $85 per barrel.

Chart 1: Estimated Fiscal Breakeven Price (USD/bbl)

*Not an OPEC member Source: IMF, Allianz Research

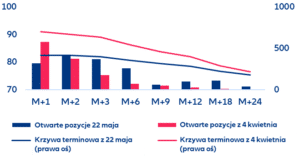

…But the group may begin to ease its supply restrictions if it decides to capitalize on the “geopolitical premium” that has recently driven oil prices higher. In early April, Brent oil prices exceeded $90 per barrel due to rising tensions between Iran and Israel. Such geopolitical risks often disrupt supply chains and create uncertainty about future supplies. However, their impact on oil prices can be short-lived. In early April, investors were mainly concerned about short-term supply, and the futures curve was in strong backwardation (i.e., oil was expected to be significantly cheaper in the coming months – see Chart 2). Indeed, after this sharp price increase, stabilization occurred as immediate threats were assessed and managed.

Chart 2: Brent Futures Curves (USD/bbl) and Open Interest (1,000 contracts)

Currently, the main drivers of (oil prices) are the Fed and the risk of higher interest rates, as well as demand concerns. Since early April, prices have dropped sharply to around $82 per barrel as of May 22, mainly due to a global oil demand decline of 1.1 million bpd from February to March 2024 to 102.3 million bpd. This decline was primarily due to lower consumption in the Middle East (-0.5 million bpd) and Europe (-0.3 million bpd). Nevertheless, robust economic growth in other regions, especially the US and Asia, helped keep demand relatively high. Going forward, markets are becoming increasingly bearish due to fears that the Fed may maintain high interest rates in the US to combat stubborn inflation, potentially reducing demand in the US and globally. Higher interest rates could also potentially strengthen the US dollar, causing oil prices to rise further, thus decreasing global demand.

Allianz Trade’s oil price forecasts remain largely unchanged as bearish and bullish signals appear to balance each other out. Looking ahead, we expect supply to remain largely at current levels, and demand to continue showing signs of slowing, especially in Europe. On the geopolitical front, we do not rule out episodes of tension but do not foresee events with a lasting impact on oil supply. As a result, Allianz Trade forecasts that oil prices will average $84 per barrel in 2024 (slightly higher than our previous forecast of $83 per barrel) and $81 per barrel in 2025 (unchanged from our previous forecast).